What’s inside?

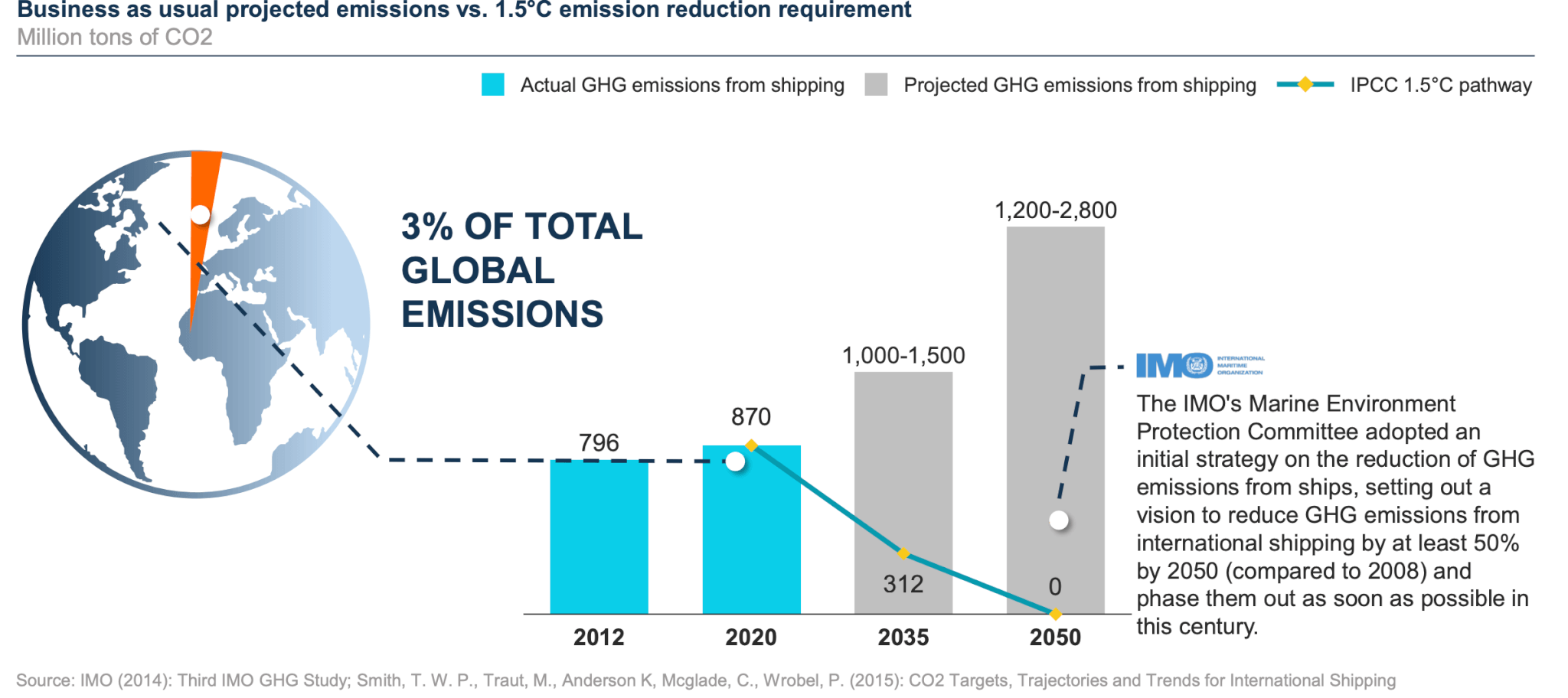

A little more than a year ago, the IPCC published the 1.5 degree report – setting a goal of “net-zero” carbon emissions by around 2050. This goal suddenly moved the need for action from the distant future to the immediate present. It also made it clear that every sector will need a strategy for complete decarbonization – there will be very little room for foot-dragging.

For shipping, this goal was translated into a 2030 target by the “getting to zero coalition”. It was launched in September at the United Nations Climate Action Summit; more than 70 organizations from across the value chain signed up, including Maersk, the Ports of Antwerp and Rotterdam, Shell and Unilever. The coalition set the target of “technically feasible, commercially viable, and safe zero emission deep sea vessels entering the global fleet by 2030”.

Towards Net-Zero

Shipping already has a broad portfolio of efficiency measures available that could be implemented immediately and profitably, as outlined in the ‘Towards Net-Zero’ report I authored with my team, and which was published last week. Slow steaming is probably the simplest, and one of the most impactful. Others include route optimization, improved hull designs, and wind assistance.

Net-zero however also means that efficiency improvements will not be enough – we will need zero carbon options like battery/electric, hydrogen and ammonia. So, over the last four months, we spoke with around 30 experts from the maritime industry, including researchers and innovators, and went through dozens of reports. From this, we distilled three focus areas for action:

- Deploy fully electric and diesel/ electric hybrids at scale (new as well as retrofits) on short distances up to ~100nm.

- Pilot hydrogen and ammonia for larger ships and the longer distances that emit about 90% of total global maritime emissions.

- Develop new business and financing models for zero-carbon fuels.

Fuel for Thought

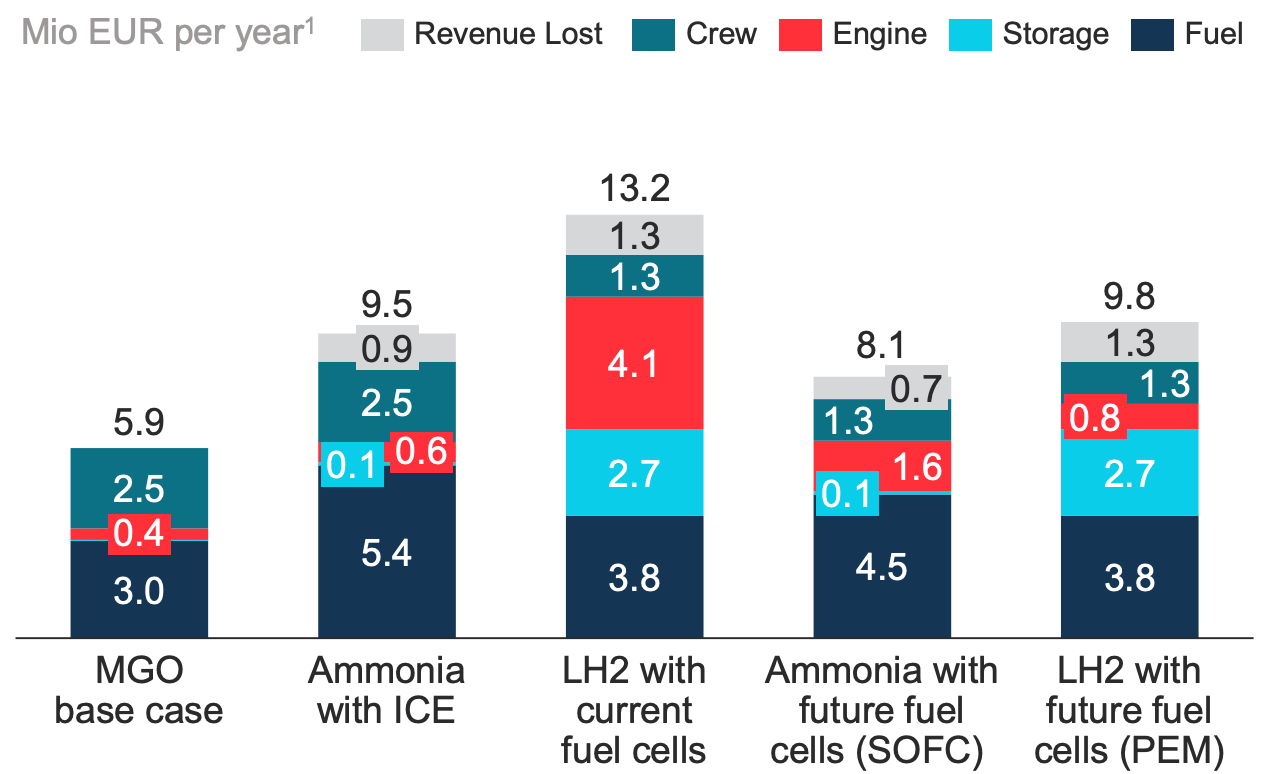

The main surprise was the economics: Battery/electric ships are already more profitable than diesel e.g. on many of the shorthaul ferries in the Nordics. Predicted costs for hydrogen and ammonia vary widely, but with a chance of cost parity with Marine Gasoil (MGO).

Interestingly, while for current Heavy Fuel Oil (HFO) and MGO engines the cost of fuel is the main cost driver, in the future there will be a much richer playground for optimization. Fuel cells, for example, have high capex cost, but higher efficiency, smaller space requirements, significantly reduced maintenance and thus crew costs, as well as potential for lifetime extension by smart load management. For hydrogen, tank costs are significant, so it could be worth adapting tank capacity for the journey, or stopping more frequently.

Examples of new business models that could benefit from these cost saving opportunities include new bunkering solutions, like containerized batteries and energy packs, or offshore hydrogen bunkering stations. Fuel cells and batteries could also enable remotely/ autonomously-controlled vessels; first design concepts already exist.

Fertilizer Fuel

A second key outcome was that ammonia deserves more attention: Ammonia has only recently entered the discussion as a potential fuel but in our view has the potential to provide a faster route to scale-up than hydrogen, as the whole production and supply chain is more mature. Ammonia as already produced at scale (140m tons a year) for the fertilizer industry and shipped globally on the seas. This also means that components like pumps, tanks, valves and the like are readily available at industrial scale and cost. Hydrogen is also already produced at scale from fossil fuels. For long distance shipping, though, liquefied hydrogen would be required, and the infrastructure and components for producing and handling it is not yet available.

Overall, we need pilots on the water. We need to test new combustion engines and fuel cells that will be coming on the market during the next five years, develop procedures for safe handling of ammonia’s toxicity and the -253 degrees of liquid hydrogen and get started on the cost reduction curve – all in time for scale-up after 2030. Pilots will also act as a signal to the rest of the value chain that will unleash investments and help regulators be transparent about the cost gaps that incentives will need to cover.

Funding to get started is available today: The EU ramped up innovation grants for the shipping sector in 2019. Forty billion euros is expected for climate-related innovation as part of the ‘Horizon Europe’ 2021-2027 program. Also national programs, venture capital funds, ship finance banks and opportunities to transfer costs to the end-customer can be tapped to close the funding gap.

Getting There

To conclude – the transition to zero-carbon fuels will certainly be challenging. Essentially, it requires building entirely new value chains from fuel supply to new shipping engines as well as the supporting financing and business models – all within the coming 10-15 years.

There are many uncertainties on technology performance and costs, the pace at which infrastructure can be developed, future carbon prices and on which technology will win.

At the same time, there is a great opportunity, not only to radically improve the environmental footprint of shipping, but also economically. One of our interview partners said that he sees the North and Baltic Sea region as the ‘Silicon Valley of zero-emission technologies’ for the shipping sector. We think the ingredients are all there: a strong ecosystem of all relevant players across the value chain, organizations and individuals willing and capable to take on the challenge, and supportive financial institutions and regulators.