What’s inside?

Ask any underwriter why the Hull & Machinery market has underperformed for so long and you’re bound to receive a variety of responses. Attritional machinery damage claims, spike losses such as the Star Centurion, and increased competition brought on by Solvency II are all often cited. However, when asked for the main contributing factor there’s little disagreement: aggregate premium for the class is too low, as are the deductibles.

In the past 12 to 18 months the market has begun to harden, providing a small amount of respite from the downward pricing trajectory. As most will agree, though, there’s still a long way to go. Given there’s no guarantee the current rating environment will continue, it seems insurers are left with two options to improve combined ratios: reduce costs and improve risk selection.

Electronic placing is widely believed to be the answer to the first. Once the policy has been digitised (handily by the broker), data entry within insurers should be dramatically reduced; efficiencies will be gained throughout the workstream. It’s also claimed the underwriting process will be faster, allowing underwriters to spend more time assessing risk, maintaining relationships, and developing new business. But given the rating environment outlined above, what’s the best way to optimise risk selection? Should niche opportunities be the sole focus and general cargo vessels be uniformly avoided? Or perhaps ‘prestigious’ accounts should be prioritised and all vessels over 20 years old should be on restricted conditions? Alas, a one-size-fits-all approach is likely to result in missed opportunities.

Data Unlimited

Underwriters have for a long time relied upon limited data to make a decision on a given risk. This approach has largely relied on combining the underwriter’s experience with the broker’s schedule (vessel type, size, age, class, flag, and value) and, depending on availability, additional information on trading patterns, charterers, maintenance budgets, and loss record. But let’s be honest, as the market has reached an all-time low, the quantity and quality of information provided has been inadequate. All things considered – especially when most of the risk is away from the berth – H&M underwriters have a tough job assessing the risk. However, since AIS began its rollout a decade ago, the ability to monitor vessels at sea has paved the way for an updated, increased understanding of risk. It’s in this particular arena that operational profiles have an important role to play. And for that we need Artificial Intelligence (AI).

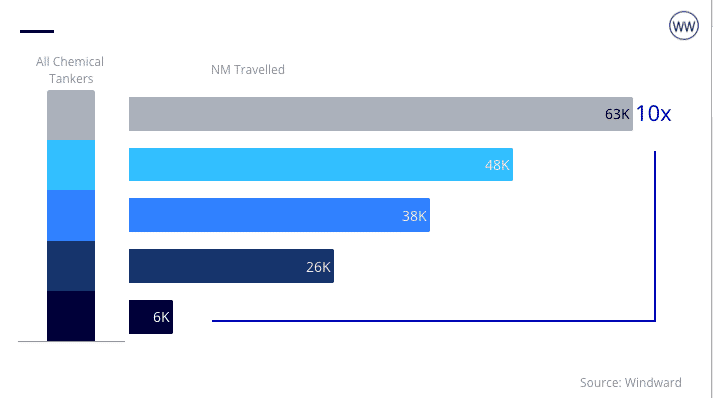

A vessel might have an adequate dollar per deadweight and total loss rating for its age, but if it’s trading twice as far as its peer group, how is the additional strain on the engines being taken into account? Or perhaps the average port approach speed of a given ship means it’s significantly more likely to experience a contact claim, putting the vessel in a whole other risk category.

Given these data points will naturally change over time, algorithms are necessary to continuously monitor for changes in a vessel’s behaviour and to recalibrate accordingly. The culmination of this should be nothing more than a data point being taken into consideration during the underwriting process; it is not the process itself.

Analytics Evolution

Using external sources of information should be nothing new, as underwriters tend to delegate elements of risk analysis to surveyors and loss prevention experts. It’s on the back of their appraisals that underwriters have made decisions on whether coverage is afforded, and if so, on what terms and under what conditions. While experts on the ground will clearly continue to have a place in the underwriting process where necessary, bringing in analytics and operational profiles to show how the vessel is operated is a natural evolution.

Gaining a deeper understanding of the risk through behavioural analytics isn’t about replacing the underwriter. Far from it. H&M insurance remains a complex class and the scope for underwriter application is immense, from understanding the underlying risk to be able to knowledgeably apply the most appropriate terms and conditions; to building strong relationships with brokers and clients to gain access to the most desirable business. Data-driven insights around a vessel’s behaviour may be providing a new way of assessing risk, but the decision on what to do with it remains firmly with the underwriters.